· Mark Davis · Operations · 13 min read

Understanding Runway and Insolvency: Why Startups Need Both Nominal and Adjusted Metrics

Discover why savvy startup leaders rely on both nominal and adjusted runway metrics to guide financial decisions. Learn how factoring in looming liabilities, understanding the difference between illiquidity and insolvency, and communicating transparently with stakeholders can help CEOs, CFOs, and board members responsibly navigate funding gaps and safeguard their startups’ futures.

For startups, financial management isn’t just a matter of counting how much cash remains in the bank. It involves understanding liquidity, liabilities, projected expenses, and the timing of large financial obligations. Two concepts that frequently arise in these discussions are nominal runway and adjusted runway. While these terms may sound like dry accounting jargon, they carry significant implications for a company’s survival. Understanding them—and the broader context of liquidity, insolvency, and fiduciary responsibilities—can be the difference between a strategic pivot and an abrupt shutdown.

In this post, we’ll break down key financial realities that face many high-growth startups and why board members, CFOs, and CEOs must embrace nuanced metrics to navigate uncertainty. We’ll explore the difference between nominal and adjusted runway, discuss insolvency versus illiquidity, and explain why reporting both runways can lead to more responsible decision-making.

Beyond a Single Runway Number

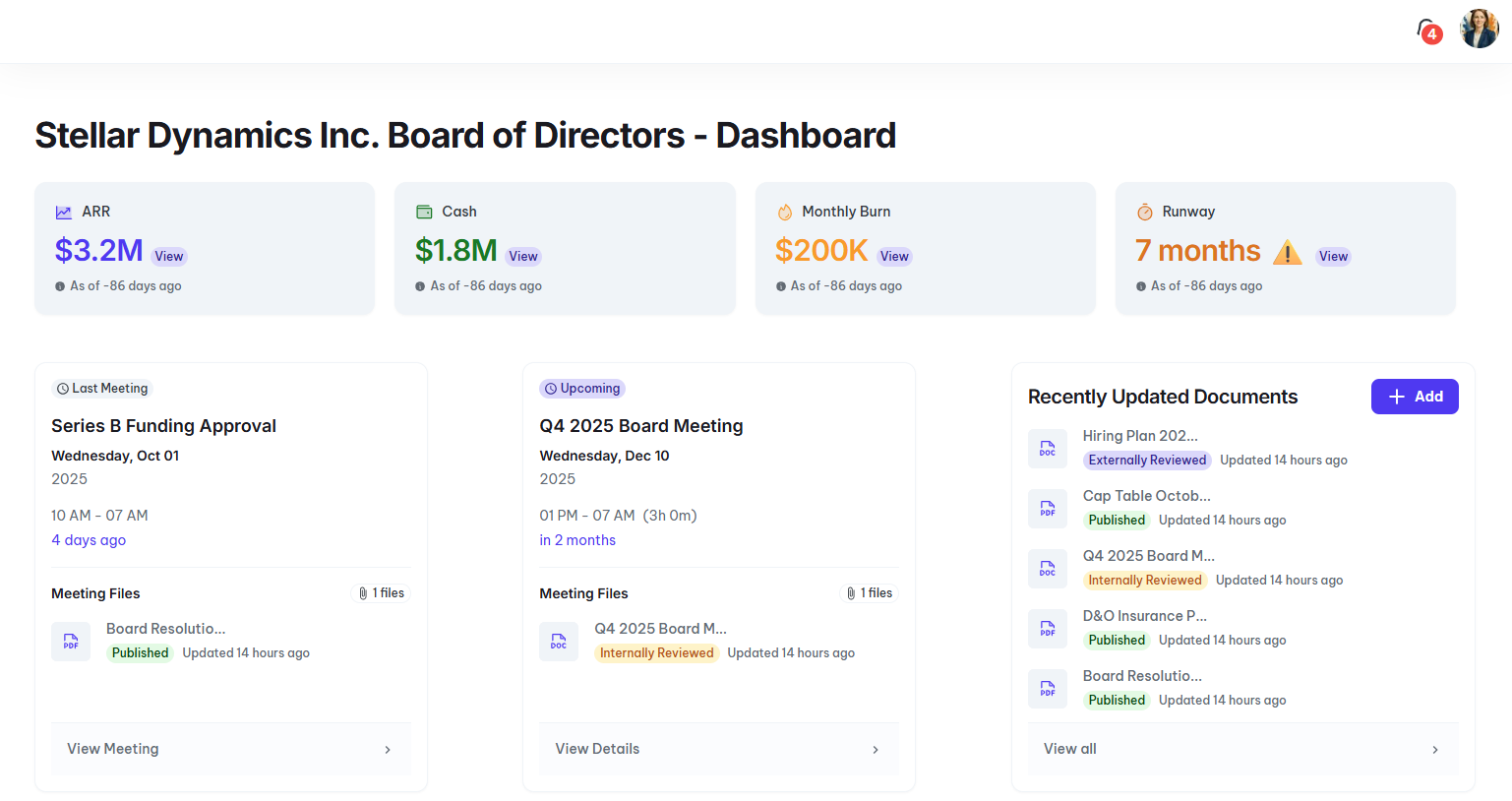

Runway is a common metric in startup boardrooms. It traditionally refers to how many months a company can continue operating at its current burn rate before it runs out of cash. Often, the simplest way to calculate it (which we’ll call the nominal runway) is to take the total cash on hand and divide it by the monthly net cash outflow. If you have $900,000 in cash and spend about $90,000 each month, your nominal runway is roughly 10 months.

But this simple calculation ignores a critical factor: the timing and magnitude of your liabilities. Are there large payables due in a few months? Has the company signed a loan agreement that will require a huge payment in six months? These are not small details. When big liabilities come due, they can dramatically shorten how long the business can truly operate.

This is where the adjusted runway comes into play. Adjusted runway accounts for all those looming obligations—the big debt payments, accounts payable, and other liabilities—that will reduce the amount of cash truly available for ordinary operations. By factoring these in, adjusted runway might be substantially shorter than the nominal figure. For instance, while your nominal runway might be 10 months, the presence of a large loan payment six months out could reduce the adjusted runway to eight—or even fewer—months.

Runway Calculator: Copyable Formulas

Use this framework in your spreadsheet. Copy these formulas and adjust for your inputs.

Basic Inputs Table

| Input | Your Value | Example |

|---|---|---|

| Cash on hand | [A] | $1,200,000 |

| Monthly burn rate | [B] | $120,000 |

| Accounts payable (current) | [C] | $85,000 |

| Debt payment due (next 12 mo) | [D] | $200,000 |

| Deferred revenue (unearned) | [E] | $50,000 |

| Expected AR collections | [F] | $30,000 |

Nominal Runway Calculation

Nominal Runway = Cash on Hand / Monthly Burn Rate

= [A] / [B]

= $1,200,000 / $120,000

= 10.0 monthsAdjusted Runway Calculation

Adjusted Cash = Cash - AP - Debt Due + Expected AR

= [A] - [C] - [D] + [F]

= $1,200,000 - $85,000 - $200,000 + $30,000

= $945,000

Adjusted Runway = Adjusted Cash / Monthly Burn Rate

= $945,000 / $120,000

= 7.9 monthsThe Gap: In this example, adjusted runway is 2.1 months shorter than nominal. That’s the difference between comfortable fundraising timeline and crisis mode.

Real-World Runway Scenarios

Here’s how runway calculations play out for three different startups:

| Scenario | Company A (Healthy) | Company B (Tight) | Company C (Crisis) |

|---|---|---|---|

| Cash | $2,000,000 | $800,000 | $400,000 |

| Monthly burn | $100,000 | $100,000 | $100,000 |

| Nominal runway | 20 months | 8 months | 4 months |

| Outstanding AP | $50,000 | $150,000 | $200,000 |

| Debt payment due | $0 | $100,000 (M6) | $150,000 (M2) |

| Adjusted cash | $1,950,000 | $550,000 | $50,000 |

| Adjusted runway | 19.5 months | 5.5 months | 0.5 months |

| Gap | 0.5 months | 2.5 months | 3.5 months |

| Situation | Comfortable | Fundraise now | Emergency mode |

Company A has minimal liabilities and can plan strategically. The small gap between nominal and adjusted runway indicates clean books.

Company B looks like they have 8 months but really only has 5.5. They should be actively fundraising now, not waiting until month 6.

Company C appears to have 4 months but after obligations, has only 2 weeks of true runway. This is a crisis requiring immediate action: bridge financing, emergency cost cuts, or wind-down planning.

Monthly Cash Flow Tracker Template

Use this format for your board reporting:

| Month | Starting Cash | Revenue | Operating Expenses | One-Time Obligations | Ending Cash | Runway (Nominal) | Runway (Adjusted) |

|---|---|---|---|---|---|---|---|

| Jan | $1,200,000 | $50,000 | $150,000 | $0 | $1,100,000 | 11.0 mo | 8.5 mo |

| Feb | $1,100,000 | $55,000 | $155,000 | $0 | $1,000,000 | 10.0 mo | 7.5 mo |

| Mar | $1,000,000 | $60,000 | $160,000 | $85,000 (AP) | $815,000 | 8.2 mo | 6.8 mo |

| Apr | $815,000 | $65,000 | $160,000 | $0 | $720,000 | 7.6 mo | 6.0 mo |

| May | $720,000 | $70,000 | $165,000 | $0 | $625,000 | 6.6 mo | 5.2 mo |

| Jun | $625,000 | $75,000 | $165,000 | $200,000 (Debt) | $335,000 | 3.7 mo | 2.9 mo |

Notice how runway drops sharply in June when the debt payment comes due. If the board only sees nominal runway, they might be surprised. Adjusted runway gives 6 months of warning.

When to Sound the Alarm

| Adjusted Runway | Status | Recommended Action |

|---|---|---|

| 18+ months | Green | Focus on growth, opportunistic fundraising |

| 12-18 months | Yellow | Begin fundraising prep, update materials |

| 6-12 months | Orange | Active fundraising, explore bridge options |

| 3-6 months | Red | Emergency mode: bridge or cut costs 30%+ |

| Under 3 months | Critical | Wind-down planning, inform stakeholders |

Illiquidity vs. Insolvency

To understand why this difference matters, let’s define some terms that are often misunderstood:

- Healthy: The company can meet its obligations comfortably and has a buffer for growth. It holds enough assets (and often enough cash) to pay off all obligations and still have positive equity. No immediate financial red flags appear on the horizon.

- Illiquid: The company may not have enough readily available cash to meet its immediate debts. However, it might still have valuable assets—think real estate, machinery, or intellectual property—that could be sold or borrowed against to raise cash. Illiquidity is a timing mismatch between when cash is needed and when cash is available.

- Insolvent: The company’s total liabilities exceed its total assets. Even if it has some cash today, on paper, it owes more than it owns. In a classic accounting sense, insolvency describes a situation where, if all debts were called in right now, the company would not be able to pay them off with its current asset base.

For established companies—like airlines with tangible airplanes, or manufacturing firms holding inventory—illiquidity and insolvency can diverge. They might be illiquid momentarily (struggling to pay this month’s bills) but still solvent because they could sell assets to raise funds. A short-term bridge loan or asset sale can resolve the cash crunch.

For startups, however, this distinction often blurs. Many young companies have few tangible assets to sell. Their “assets” often consist of intangible items: brand value, a prototype, or engineering talent. These are not easily convertible to cash in an emergency. As a result, when a startup runs out of immediate cash, it can feel like insolvency and illiquidity are one and the same event. Without substantial hard assets, a cash crunch often becomes a full-blown existential crisis.

Why Report Both Nominal and Adjusted Runway?

Nominal runway gives a snapshot of how long the company can survive if it keeps operating as it currently does, ignoring the future liabilities. It assumes a world in which large lump-sum payouts do not exist, or at least, are not an immediate concern.

Adjusted runway, on the other hand, incorporates a more realistic view. It looks ahead to major cash outflows—such as large debt repayments, big vendor invoices, or legal settlements—and includes their impact in the calculation. The result is almost always shorter, but more honest.

For the board of directors, CFOs, and CEOs, both numbers are vital. Here’s why:

- Strategic Decision-Making:

Reporting both runways illuminates how precarious the situation may be. Nominal runway shows how much operational time you have if conditions remain unchanged. Adjusted runway reveals the point at which major obligations will force a financial reckoning. Armed with both, leaders can decide whether to cut costs now, negotiate with creditors, or accelerate a fundraising round. - Fiduciary Responsibilities:

Once a company becomes insolvent—even if it can still pay bills for a few months—directors and executives may face heightened legal scrutiny. In many jurisdictions, directors must consider creditors’ interests once insolvency looms. Continuing to incur debts in this state could potentially expose board members to personal liability. Knowing the adjusted runway clarifies the timeline to this “red zone.” - Investor and Stakeholder Communication:

Presenting only a rosy, nominal runway can mislead investors and employees. By also showing adjusted runway, management demonstrates transparency, honesty, and a commitment to sound governance. This approach can preserve trust and credibility, which might be essential for future financing and negotiations. - Access to Bridge Financing or Refinancing:

Startups often hope that new funding will arrive before their runway disappears. By monitoring both runway calculations, leaders can time fundraising efforts more effectively. They might choose to secure a bridge loan now, rather than waiting until the very last minute, or adjust growth plans to ensure they reach profitability before large obligations come due.

The Reality of Startup Finance

Startup life is fraught with uncertainty. The combination of rapid growth, evolving products, and aggressive scaling often leads to razor-thin margins for error. Just looking at the nominal runway—the simplistic, linear calculation—can lull executives into a false sense of security. Conversely, focusing solely on total insolvency can cause paralysis or panic, stifling potentially productive action.

The goal is to recognize the complexity of the financial situation. Yes, on paper, you might already be insolvent if your liabilities exceed your assets. But thanks to the timing of payments, you may still have months of practical operating time—time that can be used to secure new funding, cut costs, or pivot toward a more sustainable business model. Conversely, if you ignore the underlying insolvency signs and rely solely on nominal runway, you risk walking blindly into a crisis you can’t escape.

A Call to Action for Boards, CFOs, and CEOs

For those in leadership positions, understanding and utilizing both nominal and adjusted runway metrics isn’t just an accounting exercise; it’s a strategic imperative. Consider the following next steps:

- Insist on Dual Reporting: Require that your finance team calculates and presents both nominal and adjusted runway in monthly or quarterly updates.

- Scenario Planning: Use the adjusted runway to run scenarios. What if you fail to raise new capital on time? When exactly does the big debt payment come due, and how does that affect your runway?

- Communication and Culture: Make honesty about the company’s financial state part of the culture. If employees and stakeholders see that management is realistic and proactive about financial challenges, it can maintain morale and trust.

- Governance and Compliance: Consult with legal counsel and consider the implications of insolvency. If the adjusted runway shows that insolvency is already at hand, you must understand the legal duties and personal liabilities that come with continuing operations.

Conclusion

Financial management in a startup context is about more than just a number in the bank account. By distinguishing between nominal and adjusted runway, executives can gain a more accurate picture of how long the company can operate under current conditions and when looming obligations may force difficult decisions. This nuanced understanding not only informs strategy and reduces the risk of unpleasant surprises, but also helps uphold fiduciary responsibilities and maintain trust with investors, employees, and other stakeholders.

In the high-stakes world of entrepreneurship, no single metric captures the full story. Embracing both nominal and adjusted runway is a key step toward making informed, responsible decisions that give your startup the best chance of thriving—even in the face of significant financial headwinds.

FAQ

What is the difference between nominal runway and adjusted runway for startups?

What is the difference between nominal runway and adjusted runway for startups?

Nominal runway measures months until cash depletion based on current burn rate, while adjusted runway accounts for realistic scenarios including delayed revenue, increased expenses, and funding gaps. Startups should maintain at least 18 months of adjusted runway to account for unexpected market changes and fundraising delays. According to Carta data, companies that raised with less than 6 months runway faced 40% higher dilution rates compared to those with 12+ months remaining.

When is a startup technically insolvent?

A startup becomes technically insolvent when liabilities exceed assets on the balance sheet, or when it cannot pay debts as they come due. Directors have fiduciary duties that shift from shareholders to creditors once insolvency occurs, requiring immediate action to avoid wrongful trading liability. Under Delaware law, directors can face personal liability for decisions made while knowingly operating an insolvent company. Boards should conduct formal solvency assessments quarterly when runway drops below 12 months.

How should startup boards calculate burn rate for runway projections?

Boards should calculate both gross burn rate (total monthly cash outflow) and net burn rate (monthly cash outflow minus revenue). Best practice requires modeling three scenarios: base case, conservative case with 25% revenue reduction, and stress case with 40% revenue reduction and 15% expense increases. Deloitte recommends updating burn rate calculations monthly and presenting scenario analyses to the board quarterly, with weekly monitoring when runway falls below 9 months.

What actions must startup boards take when approaching insolvency?

When runway drops below 6 months, boards must document all decisions in writing, obtain solvency opinions from financial advisors, and consider alternatives including bridge financing, asset sales, or orderly wind-down. Directors should consult legal counsel immediately to understand fiduciary duty shifts and potential personal liability. The board must prioritize creditor interests over shareholder returns once insolvency is reasonably foreseeable, and all transactions require enhanced scrutiny to avoid fraudulent conveyance claims under bankruptcy law.

Nominal runway measures how long a startup can operate based on current cash divided by average monthly burn rate, while adjusted runway accounts for upcoming obligations like debt payments, tax liabilities, and committed expenditures. Adjusted runway typically shows 15-30% less time than nominal calculations because it includes contractual obligations that will accelerate cash depletion. Boards should review both metrics monthly to avoid insolvency surprises, as relying solely on nominal runway can mask imminent cash crises.

How much runway should a startup maintain before raising additional capital?

Startups should begin fundraising when they have 9-12 months of adjusted runway remaining, not nominal runway. Enterprise fundraising rounds typically require 6-9 months to close, and unexpected delays are common. The National Venture Capital Association recommends maintaining a minimum 6-month cash buffer after accounting for all committed obligations. Starting fundraising too late forces founders into unfavorable terms or bridge financing situations that dilute existing shareholders and signal distress to potential investors.

What are the legal consequences of trading while insolvent for startup directors?

Directors who allow a company to continue operating while insolvent face personal liability for debts incurred during that period under wrongful trading laws in most jurisdictions. In the UK, the Insolvency Act 1986 holds directors personally responsible for company debts if they knew or should have known the company could not avoid insolvency. US directors face similar exposure under fraudulent transfer laws and fiduciary duty violations. Directors must document solvency assessments quarterly and cease trading immediately when adjusted runway falls below operational minimums.

How do you calculate adjusted runway for a startup?

Calculate adjusted runway by taking current cash balance, subtracting all committed obligations within 12 months including debt principal payments, tax liabilities, lease commitments, and signed vendor contracts, then dividing by average monthly operating expenses. Include a 10-15% contingency buffer for unexpected costs. For example, a startup with 500,000 in cash, 100,000 in committed obligations, and 50,000 monthly burn has 8 months adjusted runway, not the 10 months nominal runway suggests. Update this calculation monthly with actual expenditure data.

What financial metrics should startup boards monitor to prevent insolvency?

Boards must monitor adjusted runway, quick ratio (liquid assets divided by current liabilities, target above 1.0), and burn multiple (net burn divided by net new revenue) monthly. Deloitte’s 2023 Private Company Governance Survey found that 68% of failed startups had adequate nominal runway but failed to track adjusted metrics. Boards should also review accounts payable aging, covenant compliance for any debt facilities, and cash conversion cycle. Implementing a 13-week rolling cash flow forecast provides early warning of liquidity issues before insolvency occurs.

Part of our Board Member Guide — Your go-to resource for board member roles, responsibilities, and best practices.

Related Reading

- Stakeholder Communication Basics

- Common Legal Risks for Startups: What Every CEO Should Know

- Is the importance of team building reflected in your schedule?

Mark Davis

Founder, I'mBoard

Mark Davis is Founder of I'mBoard. Having served on dozens of startup boards, he knows the pains from both sides of the table - as an exited founder/CEO turned investor.